What was the lawsuit about?

The key issue in the lawsuits was the practice of “tying.” NAR members were required to include the buyer agent’s commissions at the time of the listing. So both commissions were actually set by the seller’s agent. These NAR practices dominated the realty market in the United States, as close to 90% of all homes sold are listed through a Multiple Listing Service (MLS).

Bill Gassett, a home sales expert and owner of Maximum Real Estate Exposure contributed his thoughts.

There are times in many businesses when people get comfortable with how things have always been done. I remember the early 90s when buyer’s agency arrived on the scene. There was significant panic, as there is now in the real estate industry. How can we possibly do business like this was the rallying cry. Times change, and people need to adapt. This situation is no different from many that have preceded us. Frankly, real estate commissions should be decoupled. It should have happened with the advent of buyer’s agency, but it didn’t for some reason. I am not sure it will at this point, either. Other than how the commission is communicated things may end up as business as usual for the most part. However, I would not be surprised if the Justice Department steps back in at some point and demands it.

What Did NAR agree to?

These changes include:

Prohibiting the listing of broker compensation offers in the MLS

1. Offers of compensation will no longer be communicated via any MLS. They can be shared online, printed materials, and shared through phone calls and emails. 2. MLS participants representing home buyers must now enter into written agreements with their clients before touring a home. This intends to ensure that buyers and their agents will explicitly agree on what services the agent will provide and for what compensation. These reforms aim to modernize real estate commission practices. Enhance transparency, and provide consumers with more choices and flexibility in their real estate transactions. They represent a significant departure from previous practices. They are also intended to address concerns related to what was considered to be anticompetitive behavior and a perceived lack of transparency.The Practicality of the New Process

In everyday business, a buyer’s agent will need to determine which house(s) the client wants to see. Then contact the agents representing the sellers to determine if the seller will be paying a commission. How this communication will be made is still undecided. If the listing agent says that the seller will pay a commission, the buyer agent will need to get it in writing to be able to enforce it later. What if the buyer is unable or unwilling to pay the commission? Will they continue to work with that agent? Or will they go directly to the seller’s agent? What happens to the protection the buyer agent represented for the buyer? The seller’s agent, by law, represents the seller first and foremost. The buyer is going to lose when an agent is representing both the buyer and the seller. An agent cannot both get the seller the most money for their home and get the best price for the buyer. Legally, home sellers have never been required to pay the buyer’s agent commission. However, it has been a long-time standard. In one of the recent contract changes, it must be included in the listing agreement. And then agreed to again in the purchase agreement.

Can a seller decline to pay a buyer’s agent?

A seller isn’t obligated to provide a commission for the buyer’s agent. Selling a home comes with significant expenses, notably Realtor commissions. Typically, these amount to around 5-6% of a home’s sale price. Commissions average 5.49% nationwide. This fee covers both the seller’s agent and the buyer’s agent’s commissions.

P> Not offering a commission to the buyer’s agent seems like a good way to cut these costs. But it may make your listing more difficult and therefore less attractive to potential buyers and real estate agents.

What does a buyer’s agent do?

Buyer’s agents are involved in the process from start to finish, including

- Buyer consultation

- Collect market data and recent comparables in neighborhoods you’re interested in

- Scheduling and facilitating viewings

- Research off-market opportunities to find additional suitable inventory

- Review all transaction documents in advance of writing any offer

- Writing and submitting an offer

- Advise on potential offer strategies that reflect current market conditions

- Negotiating price and contingencies

- Refer buyers to reputable local professionals (e.g., home inspectors and mortgage brokers)

- Explaining disclosures, inspections and possible pitfalls of a particular property

- Resolving issues based on due diligence findings

- Guiding buyers through the closing process.

Why did sellers typically pay both Realtor commissions?

The practice of sellers paying the buyer’s agent commission was heavily influenced by the National Association of Realtors (NAR). NAR regulations required brokers on Realtor-affiliated MLS platforms to offer compensation to the buyer.

Why was the practice of “tying” buyer and seller commissions considered harmful?

The practice of tying commissions has been shown to inhibit competition and drive-up fees. Under tying arrangements, the compensation for a buyer’s agent is established before the buyer can be sure of the quantity or quality of the services their agent will provide. Not only does this make it harder for buyers to negotiate fees, tying also means that sellers may have to offer higher commissions to maximize the chance of selling their home.

A study by economists Panle Jia Barwick, Parag A. Pathak, and Maisy Wong found that homes which failed to offer buyers’ agents at least 2.5% commission had a 5% less chance of being sold. And those that did sell would spend an average of eight additional days on the market.

The Impact of Tying

The anticompetitive impact of tying is exacerbated by several factors:

First, buyers are legally prohibited from receiving rebates on commissions in ten states. So the commission paid to buyers’ agents cannot be negotiated.

Second, many buyers were unaware of the commission levels offered by prospective home sellers. One in roughly 600 local MLSs permits brokers to publish commissions offered to buyers’ agents. This severe lack of transparency meant that home buyers may have been unaware of their agents’ incentive to steer them toward higher-commission properties. Public pressure to reform the realty market may have been stunted by perceptions about who ultimately pays for the services. Although the seller directly funded the buyer’s commission out of the proceeds from the sale, economic theory dictates that the buyer ultimately took on at least a portion of the burden. That’s because the purchase price of the home includes both commissions. Who pays the commission? The buyer or the seller? It has been a hot button issue with Realtors for years.

Are there other competition concerns unrelated to tying?

One concern is around buyers’ agents steering away from properties offered for sale outside of the MLS. Namely “for sale by owner” (FSBO) properties. Here, buyers’ agents—who often represent both buyers and sellers—have an incentive to discourage home sales that do not include a listing agent. The issue is one of liability and work load. Although dual agency is legal in most states, each party should be represented by their own agent to receive the maximum fiduciary protection.

Fiduciary Responsibility

In every real estate transaction, fiduciary responsibility is given to the party whose relationship was established first. So, when the buyer agent represents both the buyer and the seller in a FSBO, the loyalty obligation is given to the buyer first. Meaning that the seller is not necessarily fully represented.

In addition to the question of loyalty and representation, the workload needs to be addressed. Preparing a buyer or a seller for a transaction is time-intensive. Doing both at the same time and trying to represent two parties with polar goals is not an easy task. To ask a person to do twice the work without compensation – which is what a-for-sale-by-owner is doing – is unreasonable.

A La Carte Fees

An additional concern is that some state-level policies require sellers’ agents to offer a minimum level of service. This essentially prohibits sellers from offering brokers lower commissions or fees to list their homes. It also discourages consumers from pursuing “à la carte” realty services. Thirteen states and Washington D.C. have effectively banned à la carte services. In nine states, consumers can only purchase à la carte services after waiving their “right” to full-service representation. A seller should be able to pick the level of service they receive. However, in order to maximize the return on the sale, the question becomes: What service or services should be left out? Sellers are certainly going to lose out somewhere by receiving less than complete services.

What are the details of the settlement agreement?

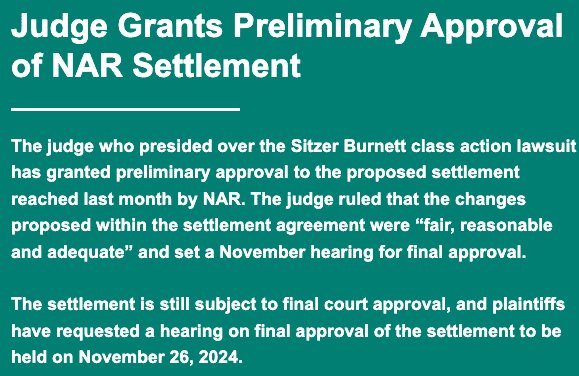

On March 15, 2024, NAR offered a settlement to resolve several lawsuits claiming that NAR’s policies drove up commission prices and harmed home sellers. The settlement comes in the wake of the October 2023 verdict in the Sitzer-Burnett case. The case directed NAR, and some of the nation’s largest real estate brokerages, to pay $1.8 billion in damages.

The Verdict

The verdict accompanies a series of similar lawsuits with targets that included NAR, regional Realtor associations, real estate brokerages, and listing services. The agreement would protect NAR and most of its members from these lawsuits and reduce the damages they must pay.

If the agreement is approved, NAR will pay $418 million in damages over four years. More importantly, tied compensation for sellers’ and buyers’ agents will no longer occur on MLSs nationwide. In anticipation of the approval, many are removing the buyer’s commission now.

Furthermore, buyers and their agents will have to explicitly agree about what services agents will provide. Since online MLS databases will no longer display commission rates. NAR will also be required to permit real estate agents to be paid for their work without subscribing to an MLS. It’s been a requirement that in order to use the “Realtor” trademark an agent has to be a member of the National Association of Realtors. It signifies a level of professionalism. Whether that is accurate or not is for another article.

What is the state of play with various lawsuits?

In addition to protecting NAR and most of its members, the proposed settlement agreement would cover many NAR-affiliated organizations, including regional Realtors’ associations. That said, the settlement does not cover all members of NAR; employees of larger brokerages and those working for corporate defendants who have not settled Sitzer-Burnett (or its many follow-ups). The agreement does provide these groups with the option to adopt the rules of the settlement and contribute to the settlement payment to be released from liability.

What does this mean for how Americans buy and sell their homes?

The outcome is unclear and will likely depend on whether the settlement is approved in a federal court. If the settlement is approved, the practice of tying will come to an end. The real estate community has been preparing for this inevitable outcome since the fall of last year. Alternative models and practices are expected to mean lower costs of housing transactions, although the magnitude is unclear.

How will this impact the U.S. economy?

Some expect that it will be treated as a gain in wealth—similar to a rise in stock prices—and would disproportionately benefit middle-class families who have an outsized share of their wealth invested in housing.However, we are not seeing a reduction in home sale prices to compensate for the switch to this new model yet. It’s too soon.

Geographic Mobility

The expected decline in the average commission could also improve geographic mobility. The “all-in” costs of buying and selling a home in the United States—including Realtor commissions, fees to lenders or mortgage brokers, charges for title services, and transfer taxes—can exceed 10% of a home’s value in some markets. Reduced mobility makes it difficult for people to relocate to areas with better jobs, limiting their lifetime earnings.”

Paul Sian, Cincinnati Northern Kentucky Real Estate agent, shared some thoughts about the recent NAR settlement: Some have been saying that the NAR settlement could result in lower prices, but I am doubtful about that. Prices are set by the buyer and seller coming together and taking account of all fees and commissions after the sale. Real estate is a very complicated transaction and, for most people is the amount of money they will spend on one thing in their lifetime. Knowledgeable buyer’s agents put in a lot of effort to help home buyers get the home of their dreams and navigate the process to ensure minimal problems. As a result, there will still be a strong need for agents who just help the buyer’s with the home buying process.So while commissions paid to buyer’s agent may not be found on the MLS that does not mean buyers will have to pay buyer’s agent directly out of their pocket.

Mobility Tax

This high transaction cost can effectively serve as a tax on mobility, which has been falling for decades. There are many factors with regard to taxes. The federal capital gains tax has not been increased in decades even though housing prices have skyrocketed to ridiculous heights. In addition, counties regularly increase rates for recording deed transfers to raise income without raising property or sales taxes. Since Covid notary fees have increased dramatically. It has become standard to send a notary to a person’s home or work rather than meeting in the escrow company offices.

Research has shown a negative association between transaction taxes and housing turnover. It indicates that lower commissions might lead to a reversal in the long-term decline in mobility. The other deterrent sellers site for their lack of mobility is that many have refinanced into mortgage rates below 3%. The cost of getting a new mortgage is thwarted by the fact that rates are now at approximately 6-7 percent. Adding to the ultra-high costs of moving.

Labor Market Impact

The impact on the labor market is unclear, especially for the nation’s roughly 2 million real estate agents. One plausible outcome might be the number of agents will decline over time. Those remaining in the realty market may take on a higher number of home transactions each year. This scenario seems likely as it becomes more difficult for inexperienced agents to have intense conversations with their clients about commissions.

Another plausible outcome is that the market experiences a boom in innovation and entrepreneurship. There are new business entrants experimenting with various models of home buying and selling.

The national conversation around real estate commissions has reached a crescendo since the National Association of REALTORS® announced a settlement agreement. This agreement would resolve litigation brought on behalf of home sellers related to broker commissions.

More Questions than Answers

Brokers and agents have their own questions about what comes next for their businesses, while at the same time fielding consumer inquiries. Many headlines aren’t separating fact from fiction, feeding misinformation. This has always been an issue in the real estate arena. The media isn’t in a position to explain a complicated and convoluted process in a sound bite.There’s no doubt the litigation—including copycat lawsuits that were filed after the Sitzer-Burnett verdict—caused considerable uncertainty. Real estate is an industry already dealing with the effects of low inventory and interest rate increases. We have been scrambling in midair. We don’t know what the rules are right now because the case hasn’t been finalized and there are regular changes in expectations.

Facts First

There’s a lot the media has gotten wrong about NAR’s settlement. Some outlets have suggested that NAR previously set or guided commissions to a standard rate of 6%. Even President Joe Biden, in recent comments, misspoke in suggesting that the settlement makes commissions negotiable for the first time. NAR does not set commissions. And commissions were negotiable long before this settlement. They are and will remain entirely negotiable between brokers and their clients. And housing prices are dictated by market forces beyond members’ control. Our job is either to get the most money for the seller or the best deal for the buyer. Getting the facts right is important, especially because the settlement agreement is complex. NAR is continuing to engage with the media to correct inaccurate reporting about the settlement. But it’s a big job. Once the incorrect information is out, you can’t un-ring the bell.

The settlement is supposed to achieve two important goals: protecting members to the greatest extent possible and preserving consumer choice. Whether it does that or not is a matter of opinion.

The proposed settlement:

The proposed settlement resolves claims against NAR and nearly every member. Including all state, territorial and local REALTOR® associations. In addition to all association-owned MLSs; and all brokerages with an NAR member as principal whose residential transaction volume in 2022 was $2 billion or below. It preserves cooperative compensation as an option for consumers looking to buy or sell a home—as long as such offers of compensation occur off of the MLS. NAR fought for a release that covered all industry players, but large settlements reached by other corporate defendants shaped the negotiations. Throughout the settlement process, NAR also engaged with a diverse range of members to consider their perspectives and interests.

“Ultimately, continuing to litigate would have hurt members and their small businesses,” NAR Interim CEO Nykia Wright said in a statement. “While there could be no perfect outcome, this agreement is the best outcome we could achieve in the circumstances. It provides a path forward for our industry, which makes up nearly one-fifth of the American economy. For over a century,” NAR has protected and advanced the right to real property ownership in this country, and we remain focused on delivering on that core mission.